Q3 2024 Investment Commentary

Macro Fall with Some Turbulence

If Gold is such a worthless rock then why do the world central banks hold so much of it?

Unraveling the Macro Map

The USA is in Macroeconomic Fall

Remember that macroeconomic fall is defined as decelerating economic growth rates and accelerating inflation rates. Moreover, this is not the same thing as recession.

On the growth side, year-over-year deceleration remains a near mathematical certainty alongside further labor market softening and another quarter of cumulative deterioration for the households and small business who are the “have nots”.

On the price side, the forces that have supported decelerating inflation rates will begin to reverse while the collective forces of US Federal Reserve policy easing, China’s recent stimulus, and a weaker USD will push up inflation rates but not growth rates. This view stands in stark contrast to the consensus view that inflation rates will continue to decelerate.

Finally, rising geopolitical tensions around the world serve as an amplification of the turbulence associated with macroeconomic fall.

USD Debasement, Deficit, and Debt

Get the direction of USD right, and you get a lot of other things right too.

The outlook for rising debt levels and deficits alongside USD debasement remains firmly entrenched across intermediate and longer time horizons. Why?

The US Federal Reserve is underway on its major easing policy pivot.

Gold is reflecting debasement far into the future.

There is no evidence of a slowdown in the continued growth of fiscal spending or the inexorable fiscal dominance that goes alongside it.

The US Presidential election appears to offer little change in that forward path as neither party appears committed in any real way to taming the debt or reining in spending/deficits.

Hard asset reflation through dollar debasement remains a principal means to hedge/benefit.

Long Emerging Markets (India)

USD debasement ignites commodity reflation which accelerates emerging market strength given that weaker USD’s boost export competitiveness, particularly among commodity producers, and the easing serviceability of USD denominated debt.

Thus, long emerging markets is simply the natural corollary to being short the USD and we'll be highlighting those countries at the intersection of a favorable macroeconomic setup and favorable bottom up confirmation from Mr. Market (India).

To be clear, as a firm policy we do not invest in China. After all, investing in communism never works.

Assuming you believe their numbers (you shouldn’t) their economy has grown 12.59% per year for 32 years. Of course, one should be super rich if you invested in such a high growth economy.

However, if you invested in the well established Shanghai Stock Exchange Index over that same period you would have annualized at 5.03% per year. Effectively, if you started with $100 then after 32 years you would have $481.61.

This compares to the USA whose economy grew at 4.58% per year and whose stock market grew 8.39% per year over the same period. Effectively, if you started with $100 then after 32 years you would have $1,320.49

As a shareholder of a company, if you are surprised that YOU don’t do well in a communist system then I have a bridge to sell you. Moreover, feel free to talk to those who invested in Russia because the stocks were cheap.

Source: TradingView

The Drakkar’s Performance and Positioning

The Drakkar: Our Multi Asset Class Long Short Longship

For a refresher on how we sail our managed portfolios, click here.

The Drakkar’s Performance

———⚜️⚜️⚜️———

The following commentary is based upon client quarterly portfolio reports and is intended as supplementary material to those reports.

———⚜️⚜️⚜️———

As a reminder, investing is just a means to an end.

That end is accomplishing your financial goals which are measured and mapped via your custom financial plan.

Every financial plan has inside of it a required return (RR) that must be earned over the long term for the portfolio to do its part in making the financial plan successful.

As such, we will compare how the managed portfolios have performed relative to their respective required return.

We will also compare the managed portfolios to a comparable diversified portfolio.

Aggressive Portfolios

Relative to the Required Return (RR)

For the quarter, our managed aggressive portfolios materially outperformed their RR benchmarks.

Year to date, our managed aggressive portfolios materially outperformed their RR benchmarks.

—————————

Relative to Comparable Portfolio Benchmarks

For the quarter, our managed aggressive portfolios marginally outperformed their aggressive portfolio benchmarks.

Year to date, our managed aggressive portfolios marginally underperformed their aggressive portfolio benchmarks.

—————————

Moderate Portfolios

Relative to the Required Return (RR)

For the quarter, our managed moderate portfolios materially outperformed their RR benchmarks.

Year to date, our managed moderate portfolios materially outperformed their RR benchmarks.

—————————

Relative to Comparable Portfolio Benchmarks

For the quarter, our managed moderate portfolios marginally underperformed their moderate portfolio benchmarks.

Year to date, our managed moderate portfolios marginally outperformed their moderate portfolio benchmarks.

—————————

Enhanced Cash Reserve Portfolios

Relative to Comparable Portfolio Benchmarks

For the quarter, our managed enhanced cash reserve portfolios marginally underperformed their cash reserve portfolio benchmarks.

Year to date, our managed enhanced cash reserve portfolios marginally underperformed their cash reserve portfolio benchmarks.

—————————

Traditional Cash Reserve Portfolios

Relative to Comparable Portfolio Benchmarks

For the quarter, our managed traditional cash reserve portfolios marginally underperformed their cash reserve portfolio benchmarks.

Year to date, our managed traditional cash reserve portfolios marginally outperformed their cash reserve portfolio benchmarks.

The Drakkar’s Positioning: The Equities

Performance

Returns in our equity positions were materially positive for the quarter and materially outperformed the global equity index benchmark which is the MSCI ACWI index.

The primary contributors to this outperformance were our exposures to

West Texas real estate where we own the oil, gas, and water rights.

Armament Industries.

India with targeted exposures to the fast growing domestic Indian consumer.

Japan with specific exposures to small companies that are highly profitable with strong balance sheets crewed by exceptional management teams.

New Positions

Updated US Large Equity Exposure

We changed our US Large Equity exposure to one that seeks to earn superior long term returns with lower downside risk by quantitatively removing overvalued low quality companies run by poor management teams. For example, these negative factors that we filter out include:

High External Financing: companies that are over reliant on external capital through high debt or stock sales.

Wealth Destroyers: companies that reinvest but generate economic returns below their cost of capital.

Value Traps: companies where intrinsic value is lower than book value; we avoid these potential value traps.

For the quarter, this strategy slightly underperformed the benchmark of US Large Companies by 0.16%.

In Q3, stocks that registered as value traps and wealth destroyers outperformed the overall market which helps explain the mild underperformance in the quarter.

Overvalued companies outperformed the S&P 500 by 2.10%.

Wealth Destroying companies outperformed by 3.97%.

High External Financing companies outperformed by 2.84%

Over the long term, we expect these characteristics will pull down return potential and as such we will continue to filter them out.

Added Japan Small Equity Exposures

This exposure is aimed at small companies in Japan that demonstrate time-tested business models and exceptional management teams that trade at attractive valuations. Moreover, these companies must show sustainable growth which should help limit downside. Furthermore, the management team responsible for the stock selection is a “feet on the street” local Japanese firm based out of Tokyo with a multi decade track record in this space.

The bottom up positive attributes the Tokyo management team is looking for include companies that have:

A well-capitalized balance sheet with little debt.

Durable competitive advantage.

High return on equity.

Above average earnings growth rate, which is sustainable and predictable.

Strong cash flow generation .

Value gap between intrinsic value and market price.

If you are interested in the Tokyo based manager’s assessment for the quarter, click here.

The top down and longer term positive attributes that we see include:

Demographic Shifts and Wealth Transfer: We expect a significant wealth transfer as Japan’s older generation passes on their savings to younger generations. This transfer, amounting to approximately $5-$6 trillion, is anticipated to boost domestic demand and economic activity as younger generations inherit and spend this wealth.

Labor Market Changes: The shift from seniority-based to merit-based pay is transforming Japan’s labor market. As the war for talent intensifies, companies are increasingly offering better pay and career opportunities to attract and retain employees. This shift is expected to enhance productivity and increase incomes, further stimulating domestic demand.

Corporate Efficiency and Profitability: Japanese companies, especially under the leadership of so-called “salaryman CEOs,” have demonstrated remarkable efficiency and profitability. Despite stagnant top-line sales since the mid-1990s, these companies have managed to significantly increase profits. This indicates strong internal management and cost-cutting capabilities, positioning them well for future growth when combined with potential new investments in technology and human capital.

These factors among many more collectively create a compelling case for the continued growth and potential of Japan’s equities market.

Source: Jesper Koll, UBS Global Wealth Report 2023, Wilkinson & Pickett & The Equality Trust, OECD, Bank of Japan, US Federal Reserve, Japan Labor Force Survey, Tokyo Stock Exchange, Bloomberg, Census Bureau, METI, Ministry of Finance, Milken Institute

Increased West Texas Real Estate Exposures

We increased our exposures to West Texas Real Estate which is specifically in the highly energy productive Permian Basin where we own not only the real estate but also the oil, gas, and water rights.

Our previous exposure consistent of approximately 870,000 acres of surface land and 2.4 million acres of mineral interests in West Texas, with a checkerboard pattern of land holdings that are effective for capturing tangential activity such as power lines, pipelines, and roadways. Moreover, this exposure is located in District 8 which is responsible for about 20% of all oil and gas production in the U.S.

Our increased exposure now includes an additional 220,000 surface acres and 8,000 gross mineral acres in the Permian Basin, with a focus on contiguous land holdings that are ideal for large-scale water management and data center operations. This offers unique advantages for data center operations (especially for AI focused workloads), including abundant and cheap natural gas for power generation, extensive water resources for cooling, and an unregulated power grid.

Finally, these exposures come with relatively low overhead costs, as these businesses do not engage directly in oil and gas production. Instead, it leases its land to producers, ensuring a steady flow of royalty income without the associated expenses and risks of production. An additional benefit is the potential for significant appreciation in the real estate itself over time, particularly as the value of energy resources increases. Additionally, the continued development and infrastructure improvements in West Texas can enhance the land’s value.

Exited Positions

Countries

Netherlands

Sectors

Utilities

Factors

US Large Equity Momentum

Maintained Positions

India

Mr. Market remains bullish on India as its world-leading economic growth is set to hold at these levels, with probabilities pointing towards accelerations in the second half of 2024.

Furthermore, we have expressed this exposure thru a “feet on the street” India based investment manager who has been around for over a decade. Their team consists of over 70 employees of which most live and work in India across Mumbai, Chennai, New Delhi, and Kolkata.

The underlying portfolio is tilted toward exposures that benefit from the growth of the domestic Indian market (as opposed to external markets via exports) and the underlying companies must meet stringent screens for management quality, business moat, growth drivers, and future potential.

Specifically, a number of factors helped propel the Indian equity market to a record high by quarter-end: a market friendly budget focused on infrastructure, employment, and consumption; continued solid foreign investor inflows; and a mildly favorable monsoon season which augurs well for agricultural production and inflation.

Our overweights in the Consumer Sectors—both Discretionary and Staples—and Communications contributed to relative performance as did avoiding the Energy Sector.

Armaments

With the rising trend of deglobalization in play combined with a rising trend in nation state geopolitical conflicts while considering that armaments spending has largely fallen to such lows implying that nation state conflict was over, the potential growth path forward is far more likely than not.

Source: Department of Defense, Worldbank, Mark Harrison “Economics of WW2”, Hedgeye Risk Management

The Drakkar’s Positioning: The Bonds

Performance

Returns in our bond positions were marginally negative for the quarter as most major bond indices posted material gains.

Our relative underperformance can be attributed to our overweight positions in short duration US Treasury Bills and our selling of call/put spreads to harvest option income.

New Positions

None

Exited Positions

None

Maintained Positions

US Treasury Bills + Option Spread Selling

We currently are maintaining our positions to US Treasury Bills which provide an excellent base layer rate of return. This combined with the overlay of option spread selling for option premium income further boosts this into the mid to high single digits over the long term.

As a reminder, selling call/put spreads is akin to selling “fire insurance” (collecting a premium of say $100) and then buying firestorm reinsurance (spending a premium of say $10) thus resulting in a net premium collection of $90 in a downside risk hedged manner. Additionally, we do it by selling short term “fire insurance” on a rolling 2 week basis i.e. our “fire insurance policies” only cover the next two weeks. Then we repeat the exercise.

It was this selling of “fire insurance” that resulted in our relative underperformance for the quarter.

Specifically, early August brought with it the unwind of the Yen carry trade.

This is a popular and very large trade where investors borrow Yen (paying Japan’s low interest rate) to invest in other currencies (or other assets) that pay higher interest rates. The Bank of Japan raised interest rates more than the market collectively expected, causing the Yen to appreciate and making the funding of the trade more expensive. Because carry trades often use copious amounts of leverage, this caused significant losses, prompting investors impacted by the trade directly to reduce exposure, which exacerbated the movement, essentially creating a classic “short squeeze.”

Ultimately, the Yen, which was down approximately 13% for the year as of early July, rallied over 12% in under a month, almost 7% in five trading days, and almost 4% in the two trading days ending August 5th, dramatic moves for a very liquid, developed market currency. In a deleveraging event, investors also reduce exposures in other parts of their portfolio, including stocks. The Japanese stock market (Nikkei 225 Index) fell by more than 12% on August 4th before subsequently rallying back to finish almost flat for the month. Other major positions reversed as well, with core bonds (the Bloomberg Aggregate) rallying over 2% in a week.

While our selling of “fire insurance” was not directly involved with the Yen carry trade, the spike in volatility was effectively a fire started in another neighborhood which then spread to the neighborhood where we had sold “fire insurance”. Thus we incurred losses.

However, our risk management process meant we always buy “firestorm reinsurance” so our losses were limited.

Still, it was during this time that the US Federal Reserve officially started cutting interest rates for the first time in years which meant anyone with bonds (especially those with long maturity bonds) experienced material gains into quarter end.

Naturally, the premiums for “fire insurance” go up materially after a recent fire which means we are earning very attractive premiums for selling “fire insurance” at this time which is more easily captured since we sell this “fire insurance” every 2 weeks and then reset.

Over the long term, we expect this systematic approach to selling short term “fire insurance” in a risk hedged manner to add material returns to our bond portfolios.

Newly Issued Agency Mortgage Back Securities (MBS)

We currently are maintaining our positions to newly issued Agency MBS.

As a reminder, Agency MBS is a pool of mortgages that is bundled together by agencies of the US Government which means they effectively have no credit risk as they are backed by the US Federal Government.

Furthermore, newly issued agency MBS means a bundle of mortgages that have been recently created.

For the quarter, this exposure did well but did underperform the broad bond index since this exposure takes less interest rate risk and has no credit risk compared to the benchmark. Again, the US Federal Reserve lowering interest rates for the first time in years meant the riskier the bond the better the bond performed into quarter end.

Still, we think it is important to take exposure when the return potential is abnormally high relative to the risk being incurred.

At this time, newly issued Agency MBS means mortgages that have just now been created with their associated interest rates of around 6% which stands in stark contrast to the majority of existing Agency MBS whose interest rates are 3% or lower. Moreover, the majority of Agency MBS exposures available to most investors is the older and inferior cohort of 3% or lower interest rates.

Relative to history, newly issued Agency MBS are paying substantially more than usual which is what attracted us to the space i.e. we love statistically high levels of compensation for a given unit of risk.

At a macro level, it is a powerful tailwind to those willing to lend for new mortgages when someone as large as the US Federal Reserve is no longer buying Agency MBS thru its quantitative easing (QE) programs. This means the largest price insensitive buyer (or lender to mortgage borrowers in this case) is no longer crowding out private capital.

The Drakkar’s Positioning: The Alternatives

Performance

Returns in our alternative positions were marginally positive for the quarter while both broad equities and bonds were materially positive .

This is all the more pleasing given that the alternatives sleeve isn’t designed to outperform or compete with equities and bonds but rather to generate return sources that are low to negatively correlated to both equities and bonds.

New Positions

None

Exited Positions

None

Maintained Positions

Trending Following Multi Asset Class Managed Futures

As a reminder, these strategies are trend followers in that they go long what is trending up and short what is trending down using price, volume, and volatility models.

The trends that can be harnessed include all the major asset classes of equities, bonds, commodities, and currencies.

Moreover, it was these strategies that materially protected our capital in 2022 when virtually every long only vanilla stock and bond investors got crushed.

Our performance can be split out into two return categories: negative performance (what pulled returns down) and positive performance (what pushed returns up).

As a reminder, a long position means you make money when prices go up and a short position means you make money when prices fall.

Negative performance:

Long

Commodities: Crude Oil

Equities: Emerging Markets

Short

Currencies: Japanese Yen

Bonds: US Treasuries, Canadian Treasuries

Positive performance:

Long

Commodities: Gold, Heating Oil

Currencies: Euro

Equities: International Developed Markets

Short

Equities: US Large Equities

Effectively, global macro markets pivoted hard with the expectation of global central banks aggressively cutting interest rates which had not been the case for the past several years.

Nevertheless, the beauty of this investment style is the ruthless execution of its quantitive rules which means there is no psychological barriers to changing one’s mind and thus positions when the data says the world is changing.

As of this writing, our updated positions are:

Long

Commodities: Live Cattle, Gold, Copper, Cocoa, Wheat, Soybean Oil, Coffee, Silver, Platinum, Natural Gas, Sugar, Soybean Meal, Palladium, WTI Crude Oil, Cotton, Lean Hogs, and Gasoline

Bonds: US 2 Year Treasuries, US 10 Year Treasuries, US 20 Year Treasuries

Currencies: None

Equities: International Developed Equities, US Large Equities, International Emerging Equities

Short

Commodities: Canola, Corn, and WTI Crude Oil

Bonds: US 2 Year Treasuries, Canadian 10 Year Treasuries, Canadian 5 Year Treasuries, Canadian 2 Year Treasuries, US 20 Year Treasuries, US 30 Year Treasuries, 3 Month SOFR, and 3 Month Corra

Currencies: Euro, Japanese Yen

Equities: None

Furthermore, there is asymmetric value in these types of strategies in the context of rising geopolitical tensions.

Let us examine how such exposures in equities, bonds, and commodities performed in multiple global kinetic conflicts like WW1, WW2, and the Korean War.

Equities

As seen in the charts below, there are a mix of equity markets that did well (naturally those countries who won) and those that did not do well (naturally those countries who lost). For bonus points, if your equity exposure was tied to producers of key war time materials (like US Steel which produced steel or Anglo-Iranian which produced oil or Vickers which produced armaments) you performed exceptionally well. This highlights the importance of being macro and historically aware when determining where to allocate equity capital.

Bonds

As seen in the charts below, the vast majority of cases show that bonds lose material value over the conflict period. This is absolutely true for the loser in the conflict and is often the case even for the victor. If you think about it, the sovereign not only drafts its people for the conflict but often drafts your money (thru inflation and debasement) to be used in the marshaling of its military so that victory can be attained. This highlights the importance of being macro and historically aware when determining where to allocate bond capital. Thus a strategy that quantitatively determines when to go long (making money when prices rise) and when to go short (making money when prices fall) is key.

Commodities

As seen in the charts below, there are dramatic commodity price moves at the onset of a kinetic conflict. Additionally, those prices often begin to materially fall once the kinetic conflict concludes. Again, a strategy that quantitatively determines when to go long (making money when prices rise) and when to go short (making money when prices fall) is key.

Source: Global Financial Data, Niall Ferguson

Gold Bullion

Gold bullion materially outperformed both broad equities and broad bonds with double digit returns for the quarter.

Gold performs exceptionally well in a macroeconomic fall weather pattern.

As seen in the charts below, you will see that

Gold demand from global central banks is accelerating at the same time US Treasuries are being reduced.

Gold demand from global central banks intensely accelerated after the start of Russia’s invasion of Ukraine.

Gold exposure is being specifically expressed via physical deliveries which highlights growing mistrust.

The top global fiat currencies (USD, EUR, GBP, CHF, JPY, etc) have all lost material value relative to gold over the past several decades with the best performing fiat of the Swiss Franc (CHF) “only” losing 93% of its value.

Over the past 109 years, the gold supply has increased from 38,387 tones in 1914 to 212,582 tonnes in 2023 which is an annualized increase of 1.59% per year which favorably compares to the USD supply of 26 billion in 1914 to 212,582 billion in 2023 which is an annualized increase of 8.61%.

Source: World Gold Council, Incrementum AG, Reuters Eikon, USGS, Federal Reserve St Louis

The Macro Situation Report

For a refresher on our analytical framework, click here.

Macro Fall with Some Turbulence

We got the mean reversion we were looking for to start the year. The stabilization regime failed to transition to cyclical escape velocity. Note that the ISM remains a relative (negative) outlier and has consistently understated official manufacturing/industrial production over the past 2 years+.

Source: Factset, Census Bureau, Hedgeye Risk Management

Source: Factset, Census Bureau, Hedgeye Risk Management

As previously stated, labor continues to decelerate.

First you reduce overtime hours

Then you cut temporary staffing

Then you cut hours for everyone else

Then you slow/stop hiring

Then quits fall as macro conditions tighten. (We are here)

Then existing labor is hoarded until protracted weakness results in payroll capitulation.

Source: Factset, BLS, Hedgeye Risk Management

Still, real final sales to domestic private purchases (the cleanest read on underlying domestic private sector demand) continues to show strength i.e. no recession.

Source: Census Bureau, Hedgeye Risk Management

Unfortunately, the quality of key macroeconomic data continues to degrade as key measurements are being downsized or eliminated due to budget constraints.

Source: Census Bureau, Hedgeye Risk Management

Furthermore, political bias remains evident across a selection of high-frequency survey data (see NFIB Survey below). Political polarization is intensifying with partisanship increasingly pervading views across life and economic dimensions. Indeed, the Confidence Spread between Democrats and Republicans made a new high in the latest month.

Source: Bloomberg, Hedgeye Risk Management

Across surveys, respondents continue to reference uncertainty surrounding the Election as a reason for canceled, paused or delayed Investment and hiring activity.

Source: Duke, Atlanta Fed, Hedgeye Risk Management

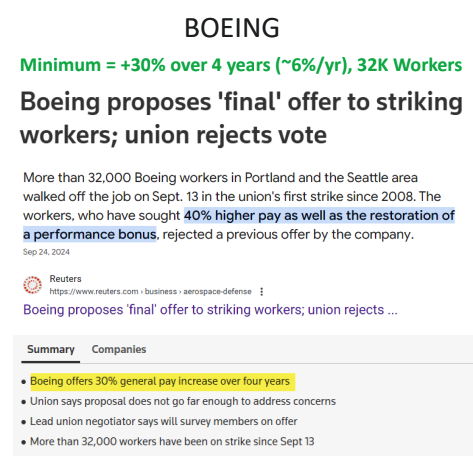

The strikes of Boeing and ILA Workers are introducing data distortions and creating a growth drag.

Roughly 47 thousand ILA Workers are directly impacted and up to 90 thousand workers in adjacent industries could be impacted under a prolonged strike scenario. The strike would need to last longer than a week to materially impact the labor data. The proactive front-loading of imports that benefited GDP in Q2/Q3 will likely reverse to a drag in Q4. When settled, roughly 80 thousand workers (ILA = 47K, BOEING = 32K) will get multiple years of 6%+ pay increases

Source: Duke, Atlanta Fed, Hedgeye Risk Management

The impending strikes were not a surprise to many. In fact, imports spiked the past few months in anticipation of the strikes. Whether it will materially blunt any negative impact remains an open question. A renormalization in the trade balance or disproportionate decline in imports could, to the extent it supports an improvement in Net Exports, benefit reported GDP Growth.

Source: Census Bureau, Hedgeye Risk Management

Naturally, mother nature has entered the game and adds her own data distortions and growth drags.

The magnitude of impact on the labor and activity data will depend on the evolution of conditions thru the NFP Survey period. Given the scope of damage and millions without power, it will manifest as a drag and, at the least, upend any clean interpretation of the data into the election. The effects are likely to be captured across a cross-section of labor data including Jobless Claims, Headline and Industry level NFP data and the Out Due To Bad Weather series among others.

Source: Duke, Atlanta Fed, Hedgeye Risk Management

Funny enough, the US Federal Reserve’s net operating loss has been dragging corporate profits lower. Specifically, the drag has been to the tune of 2%-4% since the start of the rate hike cycle. The impact isn’t overally material but the interpretation is that the underlying strength in profit growth is actually stronger ex the US Federal Reserve’s distortion.

Source: Census Bureau, Hedgeye Risk Management

Immigration has been the one distortion to dwarf them all. Specifically, immigration remains the BIGGEST KNOWN-UKNOWN in recent memory. No one has a clean read on the impact but its pervasively distorting all manner of BLS labor data.

Source: BLS, Census Bureau, CBO, Hedgeye Risk Management

Additionally, there have been massive revisions to disposable personal income, gross domestic income, and interest income to a degree that would have completely changed past prior conclusions.

Source: Census Bureau, CBO, Hedgeye Risk Management

The decline in net interest payments amidst the sharpest rate hiking cycle ever remains remarkable. Note that the first chart is in nominal dollars. On a real basis, and in the aggregate, its almost nonexistent!

In effect, Corporate America (the big firms) largely borrowed at low fixed rates during the Zero Interest Rate Policy (ZIRP) era for long periods of time (long maturity bonds) which means higher interest rates do not impact these borrowings. Combine this with companies that also have large cash balances means the interest earned on cash materially rises while interest on debt is largely unchanged.

Source: Census Bureau, CBO, Hedgeye Risk Management

Additionally, company margins may be back as growth in output prices is greater than the growth in labor costs. Also notice how company margins materially grew while labor costs also fell when China joined the World Trade Organization starting in 2001.

Source: Census Bureau, Hedgeye Risk Management

Labor momentum has clearly slowed. Core Private Sector Employment Growth (ie ex government & transfer payment linked employment) is now below 1% and is falling. Additionally, the percentage of industries reporting an increase in employment went below 50 for the first time in July and the percentage of states reporting negative changes in employment is approaching 50%.

Source: Federal Reserve, BLS, Factset, Hedgeye Risk Management

As a reminder,

The “Haves” are

The Rich who disproportionately benefit from higher rates as they get paid on their excess liquidity.

The Rich who disproportionately benefit from reflation in asset prices as they own a disproportionate share of financial assets.

The Big Banks who consolidate share amidst banking stress and liquidity flight.

The Big Businesses whose business and stock prices outperform amidst macroeconomic fall/winter uncertainty.

The “Have Nots” are

The rest who get stuck with higher (cost of living) inflation while broadly missing out on the interest income upside associated with higher rates.

The rest who lose discretionary consumption capacity as their wallet share goes to servicing higher debt costs.

The rest who become increasingly vulnerable to income shocks (ie end of student loan moratoria) as any residual cash cushion is exhausted and the above play out in reflexive and compounding fashion.

Today, cumulative deterioration remains widely evident for the “Have Nots”.

Source: Census Bureau, New York Fed, Hedgeye Risk Management

JOLTS Construction Job Openings were -177K month over month in the latest month, marking a 5th consecutive month of decline and the largest 6-month decline ever. Meanwhile, Challenger Construction Job Cut Announcements moderated in July and August but this follows -4613 in June which is the highest since the peak of the Global Financial Crisis in 2007/2008 and higher than the COVID shutdown peak in April 2020.

Source: Zillow, New York Fed, Factset, Hedgeye Risk Management

And yet it seems Wage Income Growth has remained the principal and sustainable driver of nominal growth. In fact, in mid September we saw hundreds of thousands of Amazon, Sam’s Club, Boeing, and ILA workers receive wage increases greater than 6%.

Source: BLS, Factset, Census Bureau, Hedgeye Risk Management

At the same time, we are seeing retail sales accelerating. Specifically, Redbook sales have been broadly accelerating since March and real retail sales have accelerated in recent months.

Source: Census Bureau, Hedgeye Risk Management

Alongside the Policy Pivot and falling interest rates, Mortgage Purchase Application Growth went positive for the first time in 3 years in the latest week. The % of Households expecting lower interest rates over the next year spiked to a new all time high in September.

Source: Census Bureau, Hedgeye Risk Management

With home equity at all time highs it also means the tappable equity (Home Equity Line of Credit i.e. HELOC potential) is also at all time highs.

In fact, total owners equity is greater than $35 Trillion and is up $3.2 Trillion over the past 6 months which is an increase more than 3X larger than any post global financial crisis value (excluding the peak pandemic period). Despite the fact housing equity has gone vertical, home equity loan growth has gone no where until recently. Nominal HELOC balances slouched lower from 2008 to 2022 and HELOC balances as a percentage of total housing equity remain at an all time low. USA’s domestic consumerism remains one of strongest forces in nature which means there is bullish upside asymmetry going forward and is a matter of when and not if.

Source: Census Bureau, NYFED, Federal Reserve, Hedgeye Risk Management

Fed Regional Surveys show that both prices paid and prices received continue to trend higher.

Source: Census Bureau, Hedgeye Risk Management

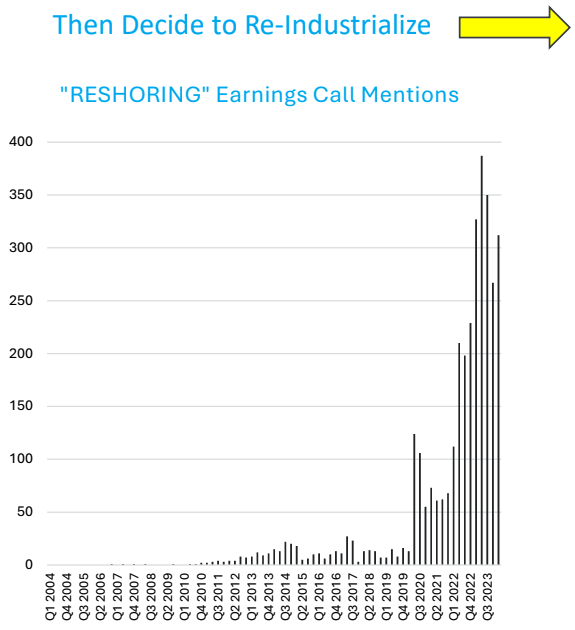

The protectionist policies, institutional distrust, civic decay, rising debt, currency debasement and intensifying geopolitical frictions all characterize Fourth Turning epochs. The real and psycho-emotional costs are high.

In fact, the path from de-globalization to re-industrialization does not solve itself in a quarter or just a year.

When you de-industrialize your local country (since you are outsourcing industrial activity to other countries like China) and then you change your mind to re-industrialize your own country but your own industrial base has eroded so much that no one remembers how to do it…well you get a spike it manufacturing labor costs.

Source: Neil Howe, Gallup, Bloomberg, GTA, Factset, Bloomberg, Federal Reserve, Hedgeye Risk Management

USD Devaluation, Deficits, and Debt

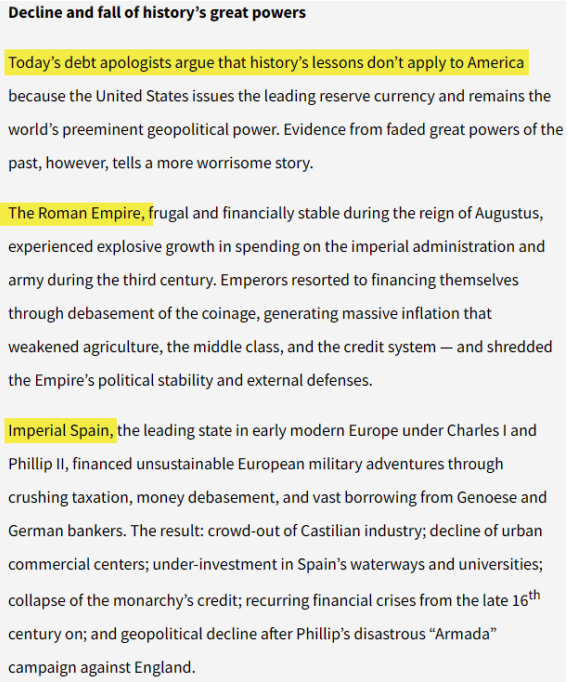

As we have stated many times before, studying the past will help you better understand the present and thus better appreciate what could be the future.

When it comes to currency debasement, the Roman Empire is a good place to start. It is all too tempting to debase the population’s currency as a means to pursue the state’s goals. Consistent abuse of the currency produced recurrent bouts of runaway inflation. Ultimately, debasement and inflation contributed to the downfall of the Empire.

Source: Visual Capitalist, Hedgeye Risk Management

Not to be outdone by the Roman Empire, the United States had its USD lose 96% of its value from 1913 through 2020, and then lost a further 18% of its value since then.

While it took the Roman Empire ~200 years (from ~70 AD to ~270 AD) to debase its Silver Denarius money by ~95%, the US managed to debase the dollar by 96% in just the 107 years from 1913 to 2020, and that’s using BLS CPI calculations which arguably significantly undercount the true level of debasement.

Source: Visual Capitalist, Hedgeye Risk Management

Source: The George W Bush Institute, ChatGPT, Hedgeye Risk Management

To be fair, the US is far from alone in debasing its currency. This table below shows debasement in local currency of countries around the world since 1999. While the US has debased the dollar by 78% or 6.3% annually since 1999, it is hardly the worst offender. Canada and South Korea have wiped out 81% and 83% of their currencies’ values, respectively. Meanwhile, more aggressive debasers like Indonesia, Brazil and China have shaved the values of their Rupiah, Real and Yuan by 91%, 95% and 96%, respectively. Russia and Argentina, of course, have gone full right tail, costing their people 99.3% and 99.9% of their currencies value.

Source: Bloomberg, Hedgeye Risk Management

Ok so it is super clear that holding large amounts of any sovereign’s currency alone is a road to impoverishment and serfdom.

This does not mean all hope is lost as there are many ways to preserve and grow one’s purchasing power.

Since 2000, the US dollar has been devalued by 6.72% per year which means $10,000 back then is equivalent to $44,710 today. Now let us compare that to gold bullion.

Since 2000, gold bullion has increased by 8.65% per year which means $10,000 of gold back then is equivalent to $67,190 of gold today.

In other words, gold bullion preserved (even increased) its purchasing power over time relative to USD because the nature of its supply is determined by nature itself and not by man.

Source: yCharts

Let us look over a longer time frame and compare USD money supply to other types of assets like US Equities and Real Estate.

Below, we see that from 1968 to the present that owning gold and US equities compounded at a faster rate relative to USD debasement which mathematically means one become truly more wealthy over time. While real estate prices went up, they did not grow at a fast enough rate which means that asset class alone experienced some debasement.

Source: Federal Reserve, PHCPI, Factset, Hedgeye Risk Management

Now you might wonder what the state of affairs are in regards to global money supply. Currently, it is accelerating past 5% per year and that is before China’s latest stimulus is captured.

Source: Bloomberg, Hedgeye Risk Management

Interestingly, American reliance on government assistance has materially increased from 1% of US counties in 1970 to 10% of US counties in 2000 to now 53% of US counties in 2022.

Source: Wall Street Journal, Economic Innovation Group, Hedgeye Risk Management

Demographically, the next two decades (2024-2050) will see the US population of 65+ grow by +36% (+22M) while the population of working age adults (20-64) will grow by 7% (+15M). This will strain government budgets. Notably, the years 2026-2031 will be particularly notable as the spread between the growth in working age and retirement age cohorts will be most acutely unfavorable, peaking in 2027-2030.

Source: CBO, Simon and Schuster, Hedgeye Risk Management

Source: CBO, Simon and Schuster, Hedgeye Risk Management

This means higher spending and higher interest will result in big and growing deficits and thus assuming falling defense spending and other mandatory spending.

Since the CBO began publishing decade-forward estimates in 2007, in comparing the period 2017-2023 to the original estimates issued in 2007-2013, the CBO has massively underestimated where Debt-to-GDP would land by an average of 32% over that time. This suggests treating the 172% estimate for 2054 with extreme caution.

Rising levels of Debt-to-GDP do correlate with slower real economic growth, especially out on the tail. While there are countries with slower growth that also have lower levels of debt, there is a striking lack of growth among countries with the highest levels of debt. Japan, Greece, Italy are all in the 0%-1.5% growth range.

Source: CBO, OECD, Hedgeye Risk Management

As such, the US Federal Reserve will be increasingly constrained by Fiscal Dominance in the years/decades ahead. If you’re not familiar with the Fiscal Dominance Theory, see below. This will form the secular inflationary runway for the next 10-20 years.

Source: CBO, Perplexity, Federal Reserve, Hedgeye Risk Management

Source: CBO, Hedgeye Risk Management

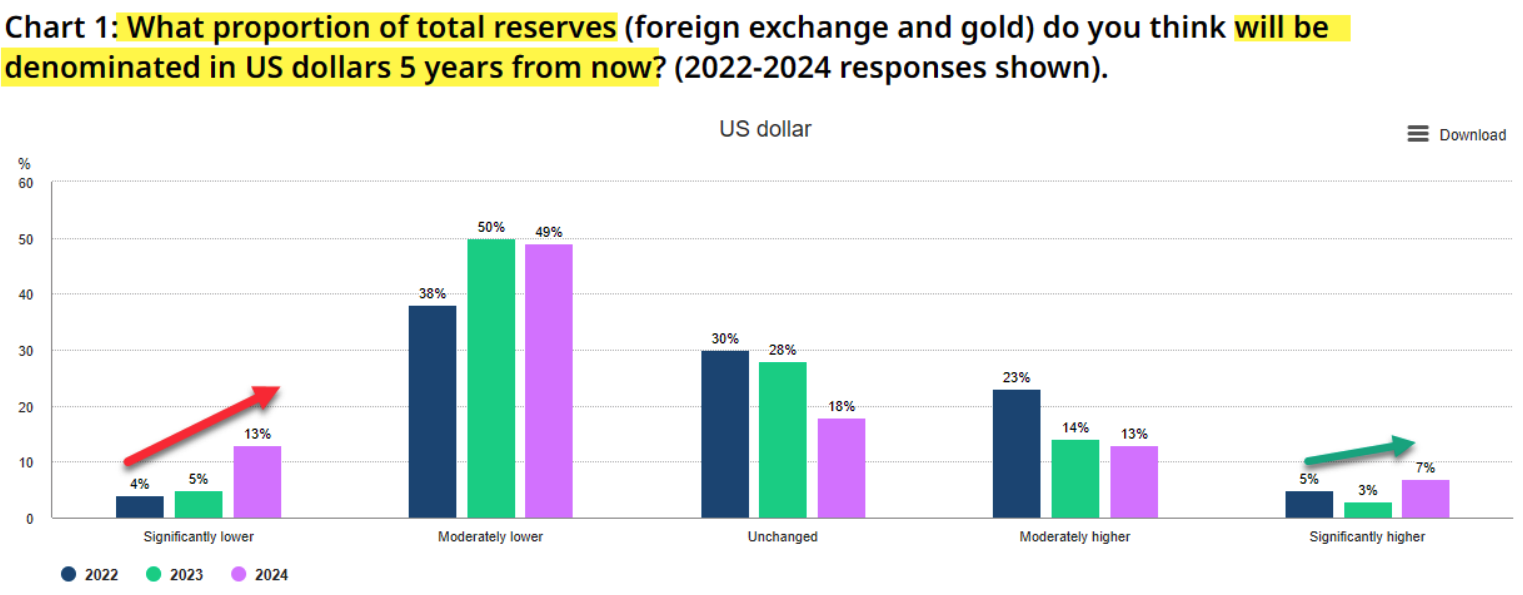

Of course, large buyers of US Treasuries are not blind. After generally rising for 40 years (1970-2008), Foreign holdings of US Treasury Debt as a % of Total have been steadily trending lower since the global financial crisis.

In a 2022 survey, 13% of Central Banks report plans to hold significantly less dollar reserves in 5 years time, up from just 5% last year. Meanwhile, the share of Central Banks planning to hold a moderately higher share of reserves in gold in five years time increased from 59% in 2023 to 66% in 2024.

Source: World Gold Council, Hedgeye Risk Management

This of course comes full circle to history.

Currency debasement, high inflation and crowding out of military spending raise the risks of (really) bad outcomes.

Source: Visual Capitalist, Hedgeye Risk Management

Long Emerging Markets (India)

As mentioned before, when USD goes down Emerging Markets tend to go up. Let us look how India has performed under those conditions.

Notice how India generally performs pretty well in a falling USD regime. Then when USD appreciates, India is still positive which stands out relative to other emerging markets.

Source: Factset, Hedgeye Risk Management

In specific reference to India.

India’s Services PMI has remained above 60 for 8 out of the last 9 months.

India missed the global industrial recession.

Source: S&P Global, Central Statistics Office of India, Hedgeye Risk Management

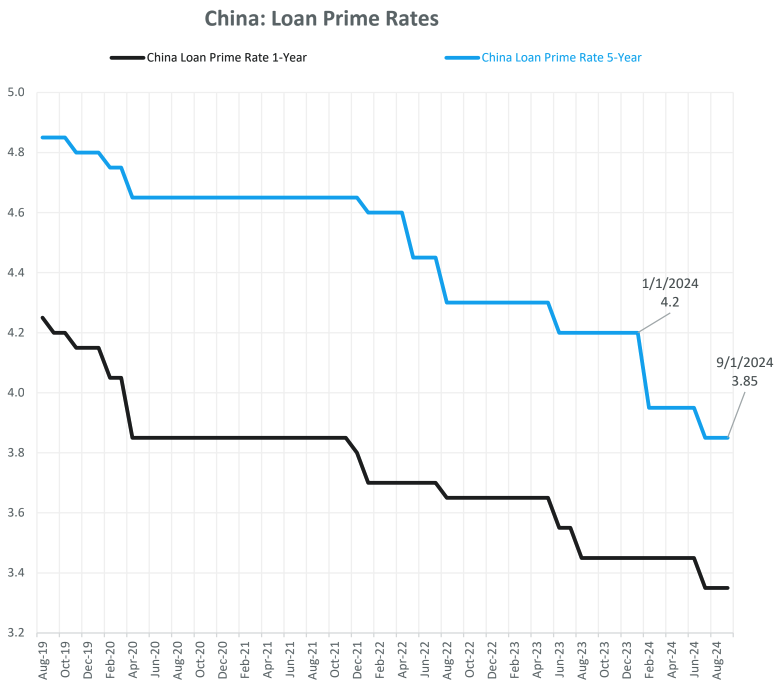

China

Let us quickly discuss China’s recent stimulus package.

China has gone from a deflationary collapse to a stimulus euphoria.

Source: People’s Bank of China, Bloomberg, Hedgeye Risk Management

Relative to the recent past, the 2024 package is more targeted, focusing on stimulating the property market, boosting consumer confidence, and shoring up the capital markets.

Source: People’s Bank of China, Bloomberg, Hedgeye Risk Management

Still, are these policies enough to overwhelm the underlying macro reality?

We think no and thus would not allocate to China but rather to India.

Outside of the risks to shareholders when investing in a communist system, the growth is weak.

Retail Sales are decelerating and historically weak.

Industrial Production is slowing and historically weak.

Manufacturing remains contractionary while services PMI rolls over.

Government relief is struggling to stop negative momentum in residential real estate.

Consumer Confidence is yet to emerge from its deep slumber.

Unemployment is increasing.

Producer prices have been deflationary from 23 straight months.

Foreign Direct Investment is in crash mode.

China credit outstanding is slo large that it is a classic case of diminishing marginal returns such that additional increases are impotent to driving the economy forward.

Source: National Bureau of Statistics China, S&P Global, China Ministry of Commerce, Hedgeye Risk Management

The information in this document is provided in good faith without any warranty and is intended for the recipient’s background information only. It does not constitute investment advice, recommendation, or an offer of any services or products for sale and is not intended to provide a sufficient basis on which to make an investment decision. It is the responsibility of any persons wishing to make a purchase to inform themselves of and observe all applicable laws and regulations.